Today, we’ll talk about how to apply for PPP Loan Forgiveness.

So we’re going to immediately assume that you know what the PPP or the Paycheck Protection Program is and you already have a loan.

So now, with the covered period ending for many small businesses, the question is, “How exactly do I go about getting the PPP Loan Forgiveness?”.

And that is exactly what we’re going to cover in this post.

So when the United States started lockdowns back in April, businesses needed a bridge to cover their costs until the economy reopened.

So many businesses, including ours, went to the banks and requested a PPP Loan.

Now, a lot of the time going into debt to survive isn’t always an attractive option.

However with the PPP Loan, if you used it to cover qualified expenses that the SBA set then you could have your loan completely forgiven.

Essentially, the loan would convert into a grant that would cover you for about 24 weeks.

That was the plan back in April 2020. Now, fast forward to November 2020 and it’s time to get our loans forgiven.

And in this post, we’re going to go over the exact steps that we are taking to get our PPP Loan Forgiven.

Also, as a disclaimer, we have to say that this is not financial advice and you should always consult with your specific accountant or lawyer.

With that being said, let’s go ahead and dive in with the first step of getting your PPP Loan Forgiveness.

How to Apply for PPP Loan Forgiveness

Step 1: You need to look at the application set-up and calculations.

Here you need to decide on your covered period and tell your lender how you’ve used your PPP funds.

Step 2: You need to go through document verification and additional questions.

In this step, you will need to upload any necessary documents to verify the information you provided and answer any additional questions required by the SBA.

Step 3: You need to thoroughly review everything, sign and submit.

Here you will review all the information that you provided, sign your PPP Loan Forgiveness application and submit it to your lender.

It’s important to know that your application will not be considered complete until it is signed.

A. When you first start your application, you’re going to want to verify your business contact information.

So at any point, if your address changed due to the shutdown and you don’t operate there anymore then you want to make sure that it is updated. Along with any phone numbers.

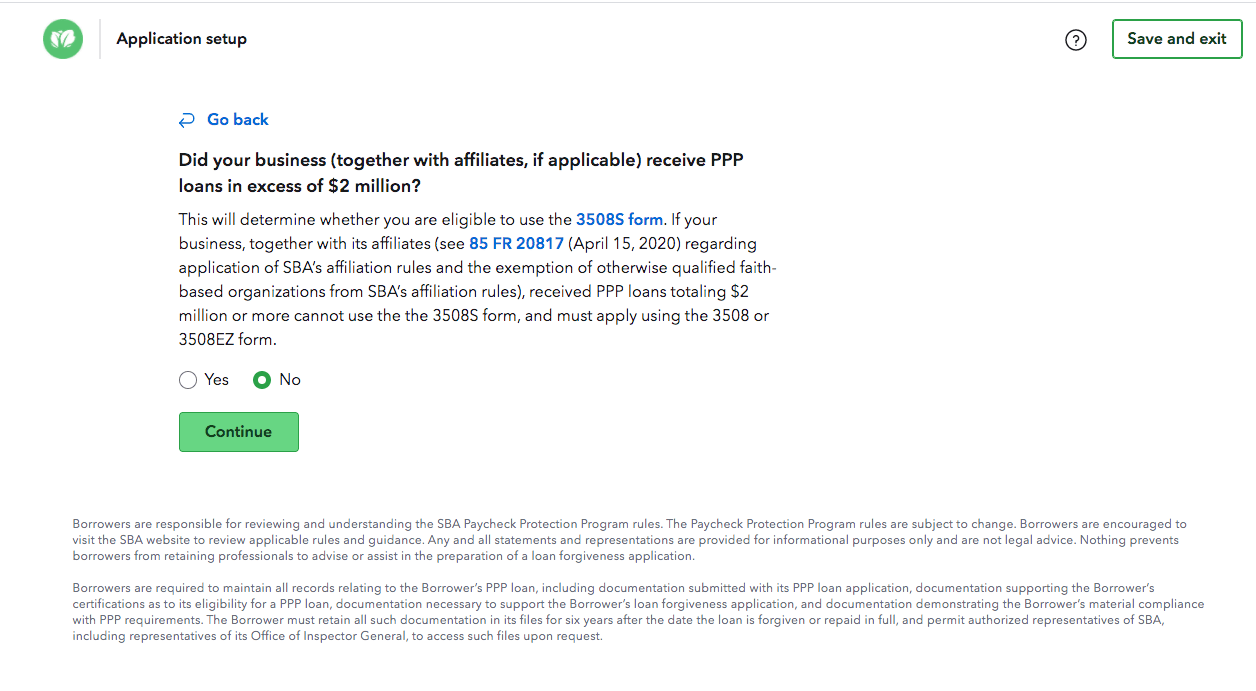

B. Next, you need to answer whether or not you received more than $2M for the PPP Loan because this will help determine which forms you need to complete.

C. After that, you’re going to have to input the date the PPP Loan arrived in your bank account. Now, this isn’t the date that you got approved, but rather when the funds arrived.

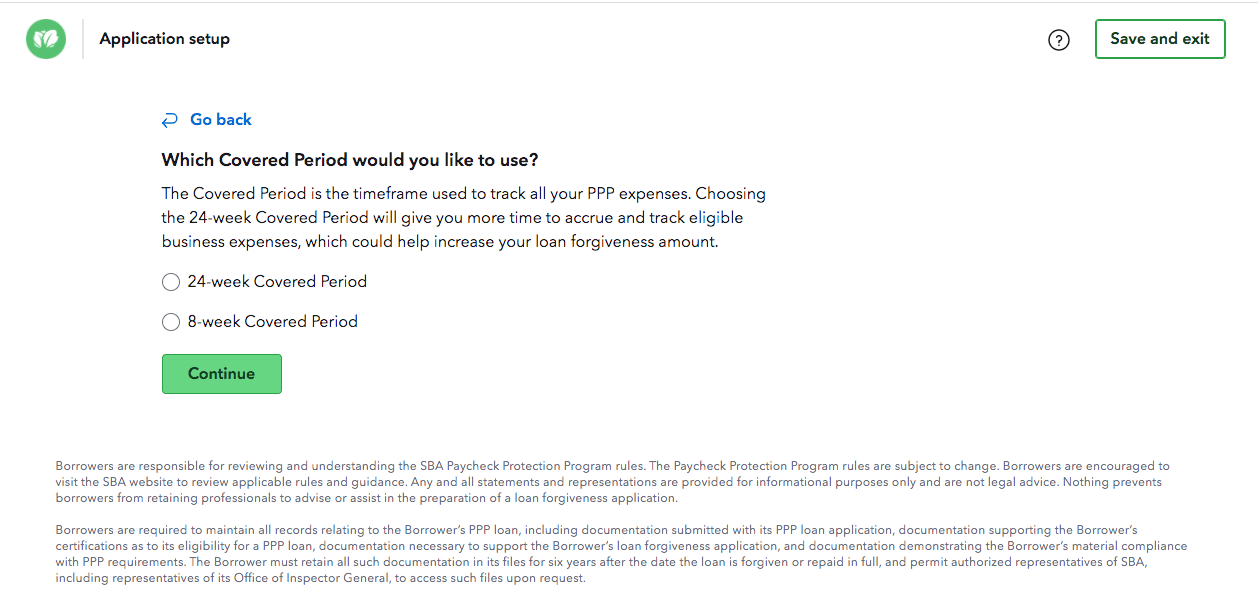

D. Next, you will want to decide on the covered period that you would like to use.

Choose between a 24 week or 8 week period.

Of course, choosing the 24-week covered period will give you more time to accrue eligible expenses, which could help increase your loan forgiveness amount.

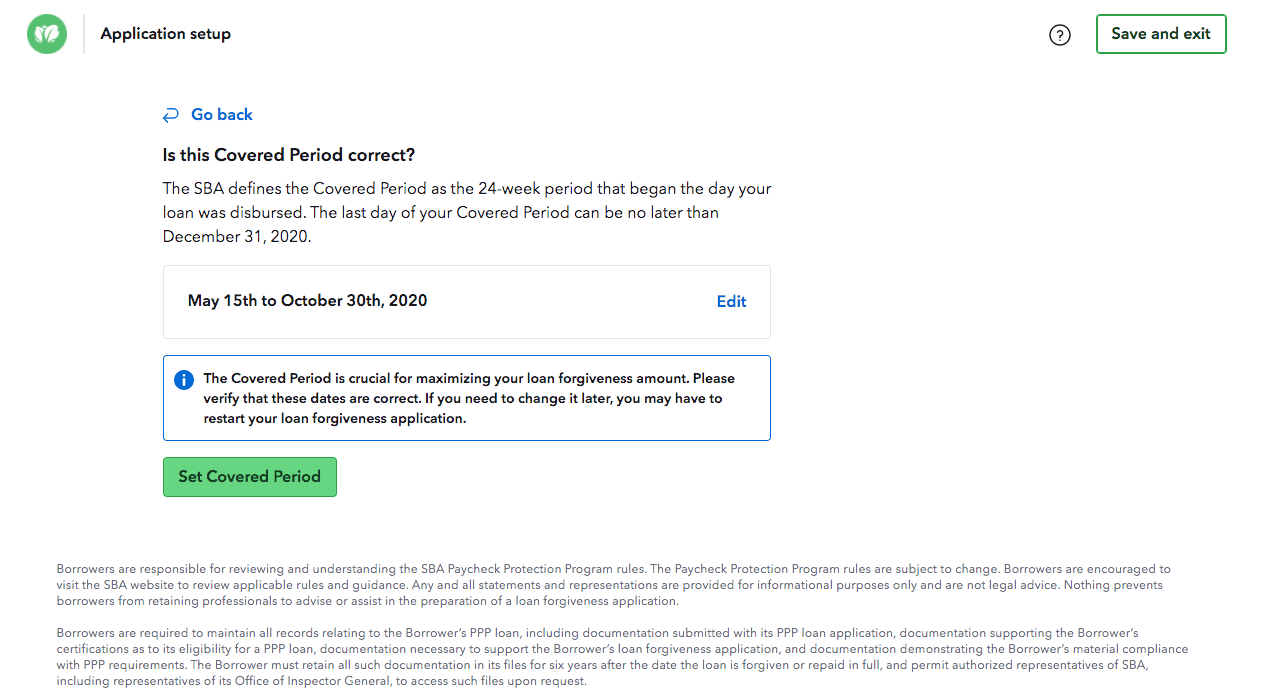

Now from the time your loan was received and the period you selected, that will determine your covered period.

For example, if you received your loan on 05/15/20 and requested a 24 week covered period then your specific cover period would be from May 15th to October 30th.

E. After that you’ll get into some more questions such as:

- What is your payroll schedule?

- Would you like to use the Alternative Payroll covered period?

Now the benefit of using an alternative payroll covered period is that you can help your covered period be aligned with your payroll schedule.

For example, if your loan was disbursed on May 15th, but your pay period begins on May 22nd.

Then the alternative payroll cover period will allow your 24-week period to start on May 22nd (as opposed to May 15th).

If you choose to use this method, then your covered period may adjust slightly.

F. After that you’re going to need to answer a few more questions such as:

- Are you self-employed? or

- Are you an independent contractor?

And if you had to reduce salary during your covered period, which if you did then it will likely affect your PPP loan forgiveness amount.

G. Next, you will need to state if your business was unable to operate at the same level of business activity before February 15, 2020?

And it’s important that it is due to compliance or guidance issued by government entities like your state or local government.

Then boom! After you’ve gone through some of those core questions, you will know which form you are eligible to use.

The SBA released a simplified, “EZ” version of the loan called “SBA Form 3508EZ” which reduces the amount of information your lender needs to process your application.

Also, you may be asked if you applied or were granted an EIDL loan which is the Economic Injury Disaster Loan.

And if you have both loans then you’re more than likely going to need to reconcile them, so you’re not getting two loans for one relief.

So if you have the PPP loan and you have the EIDL loan then your forgiveness amount is likely going to be a little bit smaller because you got paid a little bit more.

Wrapping Up

So that is how a lot of you will need to complete your PPP Loan Forgiveness application.

As we mentioned earlier in this post, applying is just the first step. After that, you’re going to need to submit accurate documentation, review, and sign.

And if you need any help with your business’ financial management or want to consult a tax expert, LYFE Accounting is what you need.

We have a professional team composed of CPAs, bookkeepers, CFOs, financial advisors, tax planners and preparers who are always ready to help you. Talk to us today!