Are you tired of paying taxes?

We share the same sentiment.

Taxes stink.

But recently, we heard that some people pay very little in taxes.

In fact, the president’s tax returns show he paid just $750 in federal income taxes in 2016 and 2017.

And nearly nothing for many years before that, according to reports from the New York Times.

Honestly, that sounds too good to be true.

So we decided to take a deeper look into it and share how you could also pay very little in taxes with real estate.

We’re going to walk you through exactly what we found and some example scenarios.

Read this whole post as today, we’re taking a look at how you can pay very little in taxes with real estate, legally.

Now we just wrote a post about the new 2021 tax brackets which you can read next.

But it’s important that you first understand how taxes work.

So by the end of this post, we expect you will know more about the tax system and what you can do to start paying less taxes.

But of course, disclaimer here, this post is not financial advice. And we always advise that you speak to your accountant or lawyer for specific recommendations for you.

Now that that’s out of the way, let’s dive in by talking about how the tax system works.

And to do this very easily, we’re going to use a fictional character through this post which we’re going to name Bob.

How the Tax System Works

Bob is a fictional corporate executive that earns $100K a year and is currently single.

And Bob wants to make smart investments with his money so that he can retire comfortably.

So let’s look at “Bob’s” tax situation.

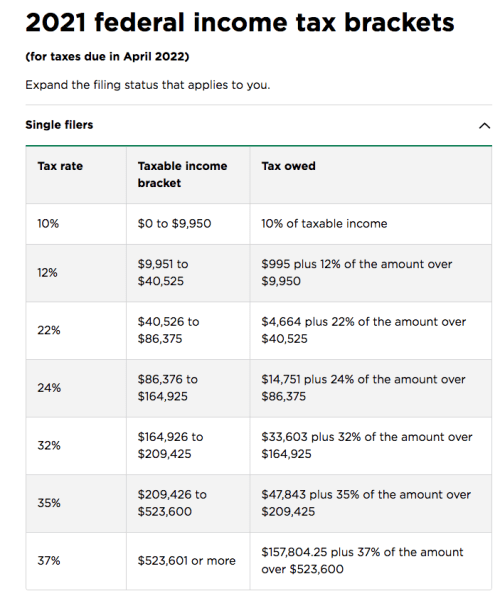

Here are the planned federal tax brackets for 2021.

Now can you guess which tax bracket Bob is in?

If you said none of the above, then you’re RIGHT!

You see even though Bob’s 100K salary fits into the 24% tax bracket, his federal taxes won’t be $24,000.

Because being “in” a tax bracket doesn’t mean that you will pay that federal income tax rate on everything you make.

The progressive tax system means that people with higher taxable incomes are subject to higher rates, and people with lower taxable incomes are subject to lower federal income tax rates.

This helps make the tax system fair.

How to Calculate Your Taxes

So Bob’s federal taxes will look more like this:

| TAX RATE | TAXABLE INCOME BRACKET | INCOME TAXED | TAX RATE | TAX OWED | TOTAL TAX |

| 10% | $0 to $9,950 | ($9950 – 0) = $9950 | 10% | $995 | $995 |

| 12% | $9,951 to $40,525 | ($40,525 – $9,951) = $30,574 | 12% | $3,669 | $995 + 3,669 = $4664 |

| 22% | $40,526 to $86,375 | ($86,375 – $40,526) = $45,849 | 22% | $10,087 | $995 + $3,669 + $10,087 = |

| 24% | $86,376 to $164,375 | ($100,000 – 86,375) = $13,625 | 24% | $3,270 | $995 + $3,667 + $10,087 + 3,270 = $18,021 |

We’ve expanded the tax brackets from earlier so that you can see how some of the math is calculated.

As you can see, even though Bob’s income is at 100K and he makes it to the 24% tax bracket, he is only taxed $13,625 at the 24% tax bracket.

And, he actually pays lower taxes in the 24% tax bracket than he would at the 12% tax bracket.

This is very important to understand because if you want to use the tax laws and system to your advantage, you have to learn how the game is played so you can maximize your chances of winning.

Know the game and increase your chances of dominating the game.

In other words, if you’re looking to pay little in taxes then you first must know how much taxes you could be paying.

Now that you know how to calculate your tax situation, let’s look at how to minimize your taxes.

How to Minimize Your Taxes

So, for the vast majority of taxpayers, the rules are straightforward.

If you earn a paycheck from an employer, odds are you elected to have your taxes withheld.

This means you are basically paying taxes that you will owe in advance.

So for every paycheck, your earnings are being reported to the government, and some, or all, of your taxes, are being paid.

But when you start making investments into business or real estate, you can optimize your tax situation.

Now the biggest thing that you need to do is reduce your taxable income.

So remember Bob’s tax bracket from earlier?

| TAX RATE | TAXABLE INCOME BRACKET | INCOME TAXED | TAX RATE | TAX OWED | TOTAL TAX |

| 10% | $0 to $9,950 | ($9950 – 0) = $9950 | 10% | $995 | $995 |

| 12% | $9,951 to $40,525 | ($40,525 – $9,951) = $30,574 | 12% | $3,669 | $995 + 3,669 = $4664 |

| 22% | $40,526 to $86,375 | ($86,375 – $40,526) = $45,849 | 22% | $10,087 | $995 + $3,669 + $10,087 = |

| 24% | $86,376 to $164,375 | ($100,000 – 86,375) = $13,625 | 24% | $3,270 | $995 + $3,667 + $10,087 + 3,270 = $18,021 |

Well, he’ll pay taxes on all the income that he makes.

But actually, thanks to the standard deduction of $12,550 as of 2021, Bob won’t pay any taxes until he makes over $12,550.

And this is probably why when you were younger and didn’t make much money, you cared less about taxes.

In fact, you probably enjoyed tax time because, with the standard deduction, you could even get a refund unless your parents claimed that from you.

Anyway, so that standard deduction is a handout that helps you reduce your taxable income.

Sounds pretty good, right?

So now, how can you get even more deductions that will reduce your income?

Now there are many ways you can do this, but in this post, let’s focus on real estate.

How to Pay Less Taxes with Real Estate

Buying and owning real estate as an investment strategy can be both satisfying and bring along tax benefits.

Going back to our fictional character, Bob.

Let’s say Bob has been studying real estate and he’s ready to become a real estate investor. His plan is to find a good property and a good tenant who would be willing to live there.

So Bob goes out, finds a single-family home that he likes, gets a loan, and closes on the home.

Now since this isn’t Bob’s primary residents, it will be treated as an investment property for tax purposes using a Schedule E.

On the schedule E, a whole new world of available tax deductions is available to Bob.

He can deduct the advertising expenses that he may use to find tenants.

He can deduct cleaning and maintenance fees.

He can deduct utility expenses, and more.

However, ideally, he’s still making some income from the property.

This means, his taxable income could potentially be even more…. Right?

Well, we particularly like two really powerful deductions for taxes with real estate.

The first one is mortgage interest.

So most people, when they take out credit cards, for example, they pay a high-interest rate. AND they can’t deduct that interest from their taxes.

But if you are a real estate investor then you can deduct that interest on any loans.

This means if you have a high enough income then your loan could almost be INTEREST-FREE with the potential of offsetting your taxable income.

That’s right, when you own a single-family home then there is going to be natural wear and tear.

The roof, the floors, and other parts will eventually start giving out.

That’s why the IRS allows you to deduct the depreciation of your home.

This alone can be enough to push you into a loss because it doesn’t directly affect your rental profits.

So Bob has been actively involved in his real estate investments and reported these “hypothetical” numbers at the end of the year.

He bought the house for $300,000

Rental income – $11,000

Mortgage insurance – $1,000

Mortgage interest – $6,000

Property taxes – $4000

Utilities – $2,500

Depreciation – $7,000

Repairs – $7,000

Rental loss – $16,500

Now if we revisit Bob’s tax situation:

His taxable income was $18,021 MINUS the standard deduction of $12,550 = leaves his tax owed at $5,471.

This is what he normally would have paid.

But since Bob is now a real estate investor, he can take this rental loss of $16,500 and deduct it against his rental income of $11,000 which wipes out that taxable income.

AND leave a $5500 loss.

Bob can apply that $5500 loss to the remaining ordinary taxable income of $5471 through a special exception to passive loss rules.

AND BANG. Bob ends up paying zero in taxes.

And the best part is that he now controls an asset worth $300,000.

So if everything hypothetically stayed the same for the use of his loan, Bob would own a $300,000 home without having to earn more or pay more in taxes.

Instead of Bob paying taxes of $18,021, he paid ZERO.

And he was able to make an investment into an asset that will increase his overall net worth.

So that’s a way to do it.

Taxes with Real Estate: Quick Takeaways

Now, this is obviously a more simplified way to minimize your taxes which works great if you make an income of $100,000 or less.

But as your income increases, you have to be willing to take on more investments in real estate or business, in order to minimize your tax liabilities.

And if you’re really looking for more ways on how you can save on your taxes with real estate or not, we have tax experts who can help you out.

From tax planning, tax preparation, tax filing, and so on, LYFE Accounting got your back. Contact us today!